Written by Hanaa Merhi

What is a caveatable interest in a property:

A caveatable interest refers to a legal or equitable interest in a property that entitles an individual to lodge a caveat with the Registrar-General. This interest serves as a notification to others that the individual has a proprietary stake in the property, preventing others from dealing with the property without their consent. It typically includes interests such as a purchaser’s interest under a sale agreement, a vendor’s lien, or a mortgagee’s or chargor’s interest.

A caveatable interest is different from a regular interest in the property. It is important to distinguish between caveatable and non-caveatable interests.

Under the Real Property Act 1900 (NSW), a person may lodge a caveat with the Registrar-General if they are entitled to a legal or equitable interest in land. As set out above, this notifies other people that you have a proprietary interest in the property and, in some circumstances, prevents others from dealing with the property without your consent. It also means the Registrar-General knows not to register any dealings, except for some statutory exceptions, that are inconsistent with your caveatable interest. This article explains how you can determine whether you have a caveatable interest in property, as well as the process for lodgement.

How can I determine if I have a caveatable interest?

A caveatable interest includes:

- a purchaser’s interest under an agreement for sale;

- a vendor’s lien;

- a purchaser’s lien;

- That of a mortgagee with an unregistered mortgage;

- On the grounds of an implied, resulting and constructive trust.

- Bankruptcy trustee interest pursuant to Section 58 of Bankruptcy Act 1966.

- Express charge clause contained in an agreement.

Only those who have an express interest in the property, such as a chargee or mortgagee, can claim a caveat. An express interest is where the parties reach an agreement for the caveat to go on the property.

What is Process for Lodging a Caveat in NSW:

A caveat can be lodged by a solicitor or conveyancer electronically with the Land Registry Services using an online platform, such as PEXA, unless an exception applies.

The caveat must be lodged in a specific form, detailing the following details:

- the title reference for the land;

- the full name of the registered proprietor(s) of the land;

- details of your caveatable interest;

- the facts on which the caveator’s claim is based, such as a fully executed contract for sale or a written agreement; and

- The signature of either the caveator or their agent. Your lawyer can also sign on your behalf.

The Most Common Caveat

The most common caveat we consider is that of a chargor or mortgagor in respect of a charge provided by the registered proprietor over the relevant land in accordance with an agreement such as a guarantee, a credit application or loan, or security deed, or a mortgage.

The most common way to way to incorporate this interest is by including a charging clause in the agreement.

What is a charging clause?

Merely being owed money does not automatically establish a caveatable interest. A charging clause is the specific wording in an agreement or contract that allows a creditor a charge over your interest in an asset. Essentially the creditor gains the status of a secured creditor or equitable mortgagee. This means that the creditor may be able to lodge a caveat or a mortgage over your property.

The Agreement should contain an operative clause under which the purchaser/customer is obliged to grant and register a caveat over the property.

There is no standard or set wording to apply a charging clause. The precise wording can differ for terms of trade, lease, guarantee, cost agreement, mortgage or commercial contract.

How do I withdraw a caveat?

In NSW, the formal withdrawal process requires the caveator to decide to withdraw their caveat. To do this, the caveator (or their solicitor) must complete and sign a withdrawal of caveat form and lodge this together with the fee.

The following individuals can also apply to withdraw the caveat:

- if joint tenants hold a caveat and one caveator dies, the surviving caveator;

- the executor, administrator or trustee of a deceased caveator;

- the Australian Securities and Investment Commission (ASIC); and

- a trustee when the caveator is an infant or is deemed mentally incapable.

This process is only suitable where the caveator wishes to withdraw the caveat. Where the registered owner, or another party with a relevant interest, wishes to remove the caveat, then the other methods set out below should be used.

Lapsing

A caveat may also be removed if it lapses. For example, this occurs when:

- the caveator’s interest is satisfied by the registration of another dealing.

- the registered owner or a party with registered interest lodges an Application for Preparation of Lapsing Notice; or

- a party lodges a dealing that the caveat prevents together with an Application for Preparation of Lapsing Notice.

The registered property owner or another interested party may typically use an Application for Preparation of Lapsing Notice to remove the caveat where the caveator will not agree to withdraw formally. The property owner may wish to register another dealing on the land, which the caveat prevents, and seek to apply for the lapsing of the caveat. You must use the relevant LPI form. Once you have lodged the form, the caveat will lapse and expire after 21 days.

Deciding on the process to remove a caveat will depend on the circumstance of your matter. As the registered proprietor of the land, you should keep in mind where:

- the caveator no longer has an interest or wishes to withdraw, they can do so by a formal withdrawal;

- you wish to remove the caveat and consider that there is unlikely to be a dispute, you should file an Application for Preparation of Lapsing Notice;

- your circumstances are urgent, or you anticipate a fight, an application to the Supreme Court may be the best option.

What Happens If a Caveat is Lodged Incorrectly?

You can only lodge a caveat if you have a caveatable interest. It’s crucial to ensure that any caveat lodged is done so with reasonable cause and a genuine belief in having a caveatable interest. Furthermore, if the court finds that the caveat was lodged incorrectly, they will remove it from the Register. As well as this, they can also order you to compensate any person that suffered financial loss due to your incorrect caveat.

Otherwise, the consequences could be severe, both legally and financially. It’s always advisable to seek legal advice before lodging a caveat to ensure that it is done correctly and lawfully.

It is emphasised that determining caveatable interest is crucial before lodging a caveat, and merely having someone owe you money doesn’t automatically grant the right to lodge a caveat.

If you require assistance with determining if you have a caveatable interest in the property, lodging or withdrawing a caveat, please contact JHK Legal on 02 8239 9600 and we will assist you,

Written by Alexander Demlakian

Within a business-to-business transaction, protecting your contractual rights is essential – especially those involving an equitable interest in land. Where a land owner may default on any contractual obligations, the second party has the right to register a caveat.

In relation to NSW, matters involving caveats involving lapsing notices are becoming more prevalent, therefore as part of our latest Insights articles, we have highlighted where these may take affect and potential steps involved in extending a caveat within the NSW courts system.

What is a Lapsing Notice?

A ‘Lapsing Notice’ is a form and legal mechanism by which registered proprietors and/or registered interest holders in a property that is affected by a caveat may make an application to the Registrar General under section 74J of the Real Property Act 1900 (NSW) (RPA) for the preparation of a lapsing notice to be served on the caveator who has lodged the caveat.

A registered proprietor or stakeholder in a property may lodge a lapsing notice for a variety of reasons. The more common reasons are that the registered proprietor challenges the underlying validity of the security interest giving rise to the lodgement of the caveat such as an incorrectly signed agreement creating the security interest or an incorrect party.

A further reason which is often utilised by a mortgagee or receiver seeking to sell a property is to lodge a lapsing notice on the basis that there is an impending sale or other dealing with the property and the caveat needs to be removed to allow settlement to proceed.

What to do when you have been served with a lapsing notice?

Firstly, you will need to decide whether or not you wish to allow the caveat to lapse or alternatively whether you would like to oppose the lapsing notice and seek to maintain your security interest and therefore your underlying caveat on the title of the property.

When you have been served with a Lapsing Notice in relation to a caveat that you have previously lodged on the title of a New South Wales property, the legislative requirements are strict and you will need to act fast if you are seeking to oppose the lapsing notice and extend the caveat protecting your underlying security interest giving rise to the lodging of the caveat.

What happens if I don’t respond to the lapsing notice?

If you do not respond to the lapsing notice, or fail to respond to the lapsing notice within the stipulated timeframe, your caveat will lapse meaning your security interest and caveat against the property will be lost and the caveat subsequently removed from the title of the property. The Court is unwaveringly strict on the adherence of deadlines in seeking to extend a caveat. Simply put, if you don’t file an application within the stipulated timeframe the Court will not consider your application.

If it is your intention to allow the caveat to lapse, then doing nothing is the most cost-effective viable option.

What do I do if I want to maintain my caveat?

It is important to note at this juncture that if you seek to oppose the lapsing notice, you will be required to commence legal proceedings in the form of an urgent application to the Supreme Court seeking in the first instance, interim orders to maintain the caveat to allow the Court to determine whether the lapsing notice should proceed, and in the second, orders to ultimately extend the caveat and seek declaratory orders as to the validity of the underlying security interest giving rise to the caveat

Issuing Correspondence to the Registered Proprietor

It is important to contact the registered proprietor or their legal representation who has issued the lapsing notice and advise of your intention to extend the caveat. This includes formally placing the registered proprietor on notice that if the lapsing notice is not withdrawn, you will be proceeding with your application to the Supreme Court to extend the caveat.

If the registered proprietor has proceeded by the appropriate path in accordance with the Supreme Court Practice Note, prior to the issuing of the lapsing notice you should have received correspondence from or on their behalf with details as to the intention to lodge a lapsing notice and detailing the grounds to do so. This correspondence would reflect the registered proprietors desire and reasoning for the removal of your caveat and either propose some form of offer to induce you to the removal of your caveat, or advising you of their intentions and position opposing your underlying security interest and therefore ultimate right to lodge a caveat.

When you receive correspondence of this nature, it is important to respond with your position as this can benefit your position in the event that you have to commence legal proceedings to extend the caveat.

Whilst the lapsing notice identifies that you have 21 days to oppose the lapsing notice and extend the caveat, it is important to understand what exactly needs to take place in those 21 days to extend the caveat.

It is a requirement in the practice note that any application for the extension of a caveat be made no less than five days before the expiration of the lapsing notice.

This means that you have until the 14th day to have issued correspondence to the registered proprietor and filed your application with the Supreme Court.

The Application & Support Affidavit

Your application to extend a caveat should be made to the Supreme Court of New South Wales pursuant to section 74K of the RPA.

The application should be made in the form of summons accompanied by a supporting affidavit.

This application is a request to the Court for an interlocutory injunction which maintains the caveat on the property and restrains the registered proprietor(s) from dealing with the land in anyway pending a trial in respect of the validity of your security interest and right to maintain your caveat.

As outlined above, when you file the Court proceedings to extend the caveat after receiving a lapsing notice, you will also need to prepare a detailed affidavit addressing your position and outlining the key facts giving rise to your underlying security interest and subsequent lodgement of your caveat this includes attaching a copy of the written agreement evidencing the security interest to your affidavit.

Court has granted Orders what do I do?

If the Court has granted you orders to extend your caveat on an interim basis, it is imperative that you must lodge these orders with the Register Generals Office via the New South Wales Land Registry Services (LRS). These orders must be lodged within 21 days of receiving the lapsing notice.

My Caveat Lapsed, What Can I Do?

In the event you failed to lodge your application in time, or a step was omitted, or an oversight occurred and your caveat subsequently lapsed either before or during proceedings it is important to be aware that your caveat can not be reinstated.

That does not mean that you do not have options available, however the Courts have been quite clear on the fact that a caveat cannot be reinstated for the same security interest on which it was initially registered nunc pro tunc (retroactively to correct an earlier ruling) see Hanover Investments v Registrar General [1999] NSWSC 21

If you are seeking to reinstate the caveat based on a security interest for which a caveat has already been lodged and then lapsed then this can only be achieved by seeking an order from the Supreme Court via an application pursuant to section 74O of the RPA.

The process of opposing a lapsing notice comes with a requirement to act very urgently and can attract significant legal costs. Should you be served with a lapsing notice, ensure that you act promptly and seek legal advice as soon as possible to ensure you are protecting your interests.

Written by George Sassine

Statutory Demands are an incredibly effective tool in ensuring companies that owe money to creditors cannot delay their payment through loopholes in our legal system. A Statutory Demand is a formal notice from a creditor to a debtor company demanding payment of a debt owed. It’s a crucial step in recovery of funds, outlining specific legal requirements for repayment.

There are serious consequences for failing to comply with a Statutory Demand and, as such, they are heavily scrutinized by the Courts. Our client’s must know how to ensure they are drafted properly and that they understand the “how’s and when’s” that a company or party may be entitled to have the statutory demand set aside and what cost consequences may flow at the expense of a client if the Statutory Demand was not issued properly.

By understanding the rules around their drafting and how they can be opposed, we can decide if they will suit our particular situations, especially if we are to engage clients looking to recover debts from companies.

Issuing Demands

As per s459E of the Corporations Act 2001 (Cth), a Statutory Demand may be issued by a person to whom a company owes a debt (or debts). As for an assigned debt, it is important to note that a debtor company must have been given notice of the debt to the debtor company under the applicable (reciprocal) legislation in each state and or territory. While this is important to keep in mind, there has been case law where it has been accepted that any notification of debt can be included with the Statutory Demand once issued.[1]

To be considered a valid Statutory Demand, a Statutory Demand, must comply with the following requirements:[2]

1. the demand must be relating to a debt that is at least $4,000.00 and is due and payable to the person making the demand;

2. Must be in writing;

3. Must specify the total amount of debt;

4. Must demand the debt is paid within twenty-one days or less;

5. Must be signed on behalf of the creditor; and

6. Must be in the correct prescribed form.

Finally, if the debt is not a judgment debt then the demand must be accompanied by an affidavit that not only verifies the debt amount that is due and payable, but it must also confirm that the demand complies with the rules provided above.[3]

If a demand is drafted in this manner, and is for a debt owing then a company may be forced to comply with the payment or enter into a suitable payment arrangement to the creditors satisfaction, if they are unable to find a valid reason for the debt to be set aside.

Additional Tips: Business owners who are concerned about cashflow should consult with their lawyers frequently to stay updated with relevant case law and precedents concerning Statutory Demands. Clear communication between the creditor and debtor and their lawyers regarding the debt can help avoid disputes and potential challenges to s Statutory Demand’s validity.

Timing is also crucial to avoid surprise and prejudice. Legal advice should be sought both in the drafting of statutory demands and in responding to any challenges or disputes raised by the debtor

Setting Aside

Generally speaking, a Statutory Demand can be set aside for four reasons. These being:

1. A genuine dispute;

2. There is an offsetting claim against the creditor;

3. There is a defect in the demand which would cause substantial injustice; and

4. Other sound reasons, especially in process.[1]

In our experience the most common of these, is that of a genuine dispute. That is, if a party who is served with a Statutory Demand is able to demonstrate that there is a “genuine dispute” regarding the debt, they may have a legal and factual basis (or bases) to have the demand set aside. Importantly, a party does not need to demonstrate that they do not owe the debt that is the subject of the Statutory Demand, but that a “genuine” dispute exists.

Further, it should be noted that the definition of a “genuine dispute” under the Corporations Act, is undefined. This means parties will need to look at the case law to understand what might be considered a “genuine dispute” for the purpose of the Corporations Act. One such example is the case of Eyota Pty Lts and Hanave Pty Ltd,[2] in which a “genuine dispute” was defined as “a plausible contention requiring investigation”, In this case the Court ruled that for a dispute to be considered genuine and sufficient it must require further investigation. This decision provides clarity and the importance on the standard required to set a aside a Statutory Demand at any time.

Statutory Demands serve as a crucial tool for creditors seeking prompt repayment by companies. Understanding the legal requirements and procedural nuances surrounding how they are issued and the challenges that they bring are essential in for both creditors and debtors. Compliance with these requirements ensures the validity of the demand and mitigates any risk of it being set aside. With careful consideration and diligence, creditors can leverage Statutory Demands to recover debts while debtors are able to defend their interests.

If you are a business owner, or a Director or Shareholder of a Company that has a debt owed to it, or has had Statutory Demand issued against it, please contact us as time is of the essence and we can assist given we have extensive knowledge and experience in this area of the law.

[1] Scolaro’s Concrete Construction Pty Ltd v Schiavello Commercial Interiors (Vic) Pty Ltd (1996) FCR 319

[2] Corporations Act 2001 (Cth) s459E.

[3] Corporations Act 2001 (Cth) s459H.

[4] Australian Beverage Distributors v The Redrock Co [2008] NSWC 3.

[5] Eyota Pty LTd v Hanave Pty Ltd (1970) 12 ACLC 669

Written by Nicola Kelso

Within the Australian financial services sector, one of the fundamental legal instruments governing the conduct of financial activities is the Australian Financial Services Licence (AFSL). From a legal perspective, understanding the intricacies of the AFSL regime is vital for businesses seeking to navigate the complex regulatory framework while ensuring compliance and managing risks.

Understanding AFSL: The Legal Side

Essentially, an AFSL is an authorisation granted by the Australian Securities and Investments Commission (ASIC) which permits a business to offer financial services to customers in Australia. In order to obtain an AFSL, businesses must follow strict rules laid out in the Corporations Act 2001 (Cth) (Corporations Act) and related regulations. These regulations set out stringent requirements relating to licencing eligibility, application procedures, ongoing compliance obligations, and enforcement mechanisms to ensure that business operate legally and ethically.

Businesses are required to hold an AFSL if the business, or part of it:

- provides financial product advice, including personal advice or general advice;

- deals in financial products, including applying for, issuing, varying or disposing of a financial product;

- makes a market for a financial product;

- operates a registered scheme;

- provides custodial or depository services, this includes if your business holds financial products on behalf of someone else;

- provides traditional trustee company services;

- provides a crowd funding service;

- provides a superannuation trustee service;

- provides a claims handling and settling service; or

- operates the business and conduct affairs of a corporate collective investment vehicle (CCIV).[1]

Whether your business falls within the scope of any of these services or the provision of these products may be unclear, in which case you may need to seek advice on the appropriateness of applying for an AFSL.

Having Your Own Licence vs. Sub-Licencing: Legal Options

The decision to obtain your own AFSL or opt for sub-licencing under another licensee requires significant consideration, tailored to the specific legal, commercial, and strategic requirements of each business.

Having Your Own Licence:

Holding your own licence provides a business with legal autonomy and responsibility over the entity’s financial operations, regulatory compliance and liabilities. This autonomy provides licensees with the ability to determine their own services, prices and business models in accordance with the requirements of the Corporations Act and the specific strategic objectives of the business, without being subject to external constraints imposed by a principal licensee. However, this autonomy comes hand in hand with increased responsibility and risks. Such responsibilities include the obligation to maintain strict compliance procedures, legal governance structures and risk management and minimalization procedures.

Sub-Licensing:

Many financial services businesses choose to operate under another licensee’s AFSL. Sub-licensee’s will benefit from a more streamlined entrance into the market along with regulatory support and operational infrastructure which is provided by the principal licensee, simplifying the complexities associated with acquiring an AFSL. However, this arrangement places a heavy dependency on compliance by the principal licensee as sub-licensee’s are bound by the terms, conditions and regulatory obligations stipulated in the principal licensee’s AFSL.

Further, the arrangement between the sub-licensee and the principal-licensee is one that is governed by a contractual arrangement. As such, businesses operating under a sub-licence must ensure that they comply with the contractual obligations of both the AFSL they are operating under in addition to the contractual obligations imposed on them under the sub-licensing agreement.

When to Get Your Own Licence:

Several reasons may prompt businesses to get their own AFSL rather than choosing to sub-licence from a principal licensee. These considerations may include:

- Expanding Services: Entities seeking to offer a wider range of financial services beyond what their current licence allows may wish to acquire their own AFSL to allow for additional activities and products within their business structure.

- Meeting Client Expectations: Some clients, including high net-worth clients and institutional investors, may prefer to work with businesses that have their own licence for credibility and security reasons.

- Ensuring Long-Term Viability: Having their own licence can signal stability and commitment to clients and investors in addition to offering greater control and resilience among regulatory uncertainties and challenges.

- Legal Autonomy: Businesses wishing to have greater control over their operations, compliance frameworks and client relationships may opt for their own licence to reduce dependencies and streamline decision-making processes.

- Risk Management: Owning an AFSL allows businesses to manage legal risks and exposure inherent in the provision of financial services more effectively by having full control over compliance.

Risks of Having Your Own Licence:

While having an AFSL provides autonomy and control, it also exposes business to inherent risks and challenges to consider:

- Compliance Burdens: Keeping up with legal requirements can be complex and expensive, requiring ongoing vigilance and investment in compliance infrastructure to ensure adherence to evolving standards.

- Operational costs: Acquiring and maintaining an AFSL involves significant upfront fees and ongoing expenses, including application fees, compliance resources and regulatory reporting obligations, which can place a strain on financial resources, particularly for smaller businesses.

- Reputational Risk: Legal breaches or misconduct can damage a business’s reputation.

- Enforcement Actions: Non-compliance with AFSL obligations may expose businesses to regulatory sanctions, legal proceedings and reputational damage, requiring robust risk management and governance procedures are in place.

- Market Dynamics: Legal changes and industry trends can impact businesses, requiring them to adapt quickly in order for effectively navigate changing consumer preferences, technological advancements and regulatory reforms.

Navigating AFSL with Legal Awareness

Navigating the complexities of the AFSL requires a nuanced understanding and consideration of the legal requirements, strategic priorities and risks inherent in the provision of financial services in Australia. Whether opting for holding your own AFSL or sub-licensing under another licensee, businesses must assess the benefits, implications and obligations associated with each approach. While holding an AFSL offers autonomy and control, it also involves significant responsibilities and risks, highlighting the importance of prudent decision making, strong compliance frameworks and risk management procedures in order for a business to thrive in the ever-changing financial services industry.

[1] Australian Securities and Investments Commission, REGULATORY GUIDE 36: Licensing: Financial product advice and dealing (June 2016) RG 36.2.

Written by Kristina Stevens

Just like Sinner, the newcomer, cleaned up the Aussie Open, so too are Queensland buyers poised to be acing the game now that their search costs have been served to sellers.

The proposed new Seller Disclosure Statement (“SDS”) under the new Property Law Act (Qld) 2023 (“PLA”) and its regulations (yet to be promulgated) provide that a SDS must be prepared by a seller and given to a buyer before the buyer enters into a contract for the sale of a lot (exceptions apply).

Presently, in addition to common law rights and specific legislative protections, the REIQ contract contains contractual warranties by a seller (for example – warranties with respect to the existence of obligations under environmental legislation) and it is the buyer’s obligation to undertake searches and make enquiries to ensure that those warranties made by the seller are true. Using the above example, unless a buyer undertakes certain searches, they will have no way of knowing whether or not the property is affected by undisclosed “notifiable activities”. These are activities that have the potential to cause contamination to land, for example, asbestos disposal. (Intensia Pty Ltd v Nichols Constructions Pty Ltd, 2018). Only if a buyer conducts the appropriate search (at their cost) and uncovers that a seller’s warranty has been breached, may the buyer be granted a termination right under the contract.

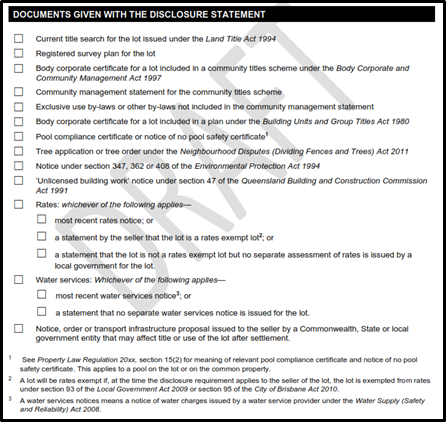

Imminently with the new regulations, the seller, prior to a buyer even signing a contract, will have to pay for, provide and attach current searches to a SDS (See Fig. 1).

Figure 1 Documents (to be) Given with the Disclosure Statement from Draft Seller’s Disclosure Notice (Queensland Government, 2022)

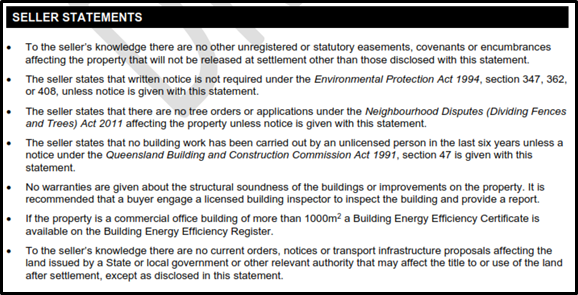

Additionally, a seller will also have to provide “Seller Statements” (see Fig. 2) as part of the SDS with respect to several matters, including: easements, written notices under environmental legislation, tree orders, dividing fences, unlicensed building work, building efficiency (in the case of commercial properties), and even transport infrastructure proposals.

Figure 2 Seller Statements from Draft Seller’s Disclosure Notice (Queensland Government, 2022)

What does this mean for your average Queensland investor?

According to the explanatory memorandum to the PLA, the purpose of the SDS introduction was to “to simplify and consolidate the disclosure process for sales of freehold land and empower prospective buyers to make informed decisions to purchase” (Queensland Government, 2023).

The new disclosure regime may make selling property, which is subject to certain defects in title or quality of title more difficult for sellers, but it will ensure that buyers are better protected and are making informed decisions as to whether or not to contract with a seller with respect to a certain property. By having the information up front, relevant to say, environmental protection or assessments, a buyer may elect not to proceed with signing a contract for the purchase of an affected property.

The proposed disclosure requirements of the SDS does not cover all searches a buyer should undertake and will not replace the requirement for a buyer’s solicitor to undertake their due diligence. The role of the solicitor will become even more relevant to assist buyers in discerning which searches ought to be undertaken that are not captured within a SDS.

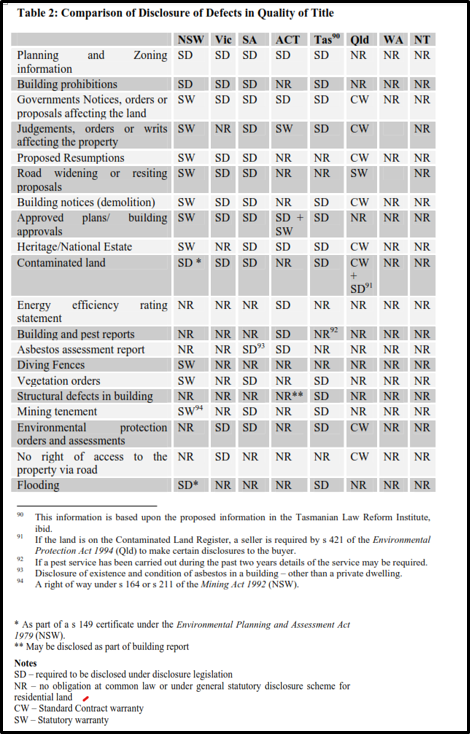

To add to the confusion, there are extensive inconsistencies across the various Australian jurisdictions in terms of disclosure requirements (See Fig. 3 ). In the author’s opinion, there is a need for discussion regarding a nationally consistent approach to disclosure. Furthermore, it has been suggested that we should investigate using technology to enable greater coordination; even potentially, a single search portal for government information (Duncan, et al., 2017). Deploying this Australia-wide, could result in uniformity of disclosure requirements in each of its states and territories. Imagine a PEXA for searches! If this information could be accessed by buyer and seller alike for a reasonable fee, it would eliminate or at least reduce placing the financial burden on either party.

Figure 3 Jurisdiction Comparison of Defects (Christensen, Duncan, & Stickley, 2017)

Until such a national approach is applied, gone are the days, where a seller’s costs and outlays were less than a buyer’s, at least in Queensland. Not unlike the Aussie Open, under the new Property Law Act (Qld) 2023, the Seller Disclosure Statement has declared there can only be one winner, and it’s the buyer taking the big trophy home.

References

Christensen, S., Duncan, W. D., & Stickley, A. (2017). Evaluating Information Disclosure to Buyers of real estate – Useful or merely adding to the confusion and expense? Brisbane: QUT Law Journal.

Duncan, W., Christensen, S., Dixon, W., Window, M., Rivera, R., & Partridge, T. (2017). Final Report: Seller Disclosure Queensland. Brisbane: Commercial and Property Law Research Centre, QUT Law.

Intensia Pty Ltd v Nichols Constructions Pty Ltd, [2018] QCA 191 [2018] 34 QLR (Supreme Court: Court of Appeal August 17, 2018).

Queensland Government. (2022). Seller Disclosure Statement – Draft. Justice and Attorney-General, Brisbane. Retrieved from https://www.publications.qld.gov.au/ckan-publications-attachments-prod/resources/edd4dab5-d833-4a04-a22e-27809fea47f9/draft-disclosure-statement.pdf?ETag=8826626087559810ff17913cd456d7ea

Queensland Government. (2023). Property Law Bill 2023 – Explanatory Notes. Brisbane.

Written by Jitesh Billimoria

Love Insurance or Separation Shield – What is this? How do you get it? Should you have it?

Insurances such as life insurance, motor vehicle insurance, building and/or contents insurance, disability insurance, and income protection are often pivotal to life’s circumstances. But where does “Love Insurance” come into the mix you may ask?

This is an intriguing question that a lot of people don’t consider but when they do, it is often too late – regret follows in hindsight and that regret is, “I should have considered getting Love Insurance“.

What is a Financial Agreement?

As American statesman, Benjamin Franklin once stated “in this world, nothing is certain except death and taxes”.

In Australia, the divorce rate averages between 40-45%, and as such, it is quite likely that you either know of someone who has divorced or you yourself may have experienced such. This rate does not include the breakdown of de-facto relationships either.

We have insurance for a variety of circumstances, in which we may not benefit but beneficiaries will. So then, why do we overlook the necessity for Love Insurance?

Isn’t protection, just like other insurance, a calculated risk, better than cure?

You should be asking then why don’t I have a ‘Separation Shield’ as my protection mechanism?

It is often believed when in a relationship that if you don’t have a substantial portfolio of assets, then a Prenuptial Agreement or Financial Agreement is not necessary. To the contrary, such Agreement can be vital in clarifying financial expectations, roles and debts, and responsibilities within a relationship. Even more so in these times, where breakdown of relationships are more prevalent and where parties leave relationships in a greater hurry compared to our parents’ generation.

Financial Agreements are designed to protect parties who are either considering marriage or are in a marriage. Similarly, those entering into a de-facto relationship or who are in one can also utilise this type of Agreement.

Why a Financial Agreement Could be Important

Over the last two decades, as people are entering matrimonial or de-facto relationships later in life, they have more assets that need protecting. Some even have to consider children from previous relationships when they enter into new relationships.

Understandably, whilst the thought of having to discuss one’s financial circumstances with a loved one may feel uncomfortable, it is essential in terms of establishing trust and transparency between the parties from the onset.

A breakdown in a relationship is often coupled with huge emotional and financial costs, and particularly if that breakdown leads to litigation. Having a Financial Agreement in place ensures clarity in respect of who owns what, when and how. It brings peace of mind that assets of both parties are protected where possible and there are clear intentions, which can reduce worry and confusion.

It captures the essence of the parties’ financial circumstances in terms of what assets, liabilities and financial resources each party brings to the relationship and accommodates any inheritance either party has received or is likely to receive.

For example, if a party has received a significant inheritance prior to commencement of the relationship, the Agreement can record and protect that inheritance from becoming joint relationship property in the event of a breakdown.

Similarly, if a party receives a significant inheritance during a relationship, would the receiving part want that inheritance available for division between the parties in the event of a separation or rather have it protected? We know most, if not all, would say that it be protected. However, if there is no ‘Love Insurance’ or a ‘Separation Shield’, then that inheritance will not be protected.

One can also deal with a number of different items in the Agreement, including: businesses, properties, spousal maintenance, superannuation, and collections (wine, shoes, classic cars, memorabilia, and other specific items). Significantly detailed Agreements can potentially highlight who pays what household expenses, how any joint-named real estate shall be purchased and dealt with at separation, and in the instance of blended family arrangements, who would pay for the damage to the property by one’s child/children.

It should be noted that each party will be required to seek independent legal advice if they are to enter into an Agreement.

For More Information

Having now read a little about ‘Love Insurance’, if you haven’t got such insurance in place and would be interested in discussing further, please contact our office on (07) 3859 4500 or via contact@jhklegal.com.au to arrange a confidential discussion as to how we can help you put appropriate steps in place.

Written by Vince Pignalosa

What is a Shareholder Agreement?

A shareholder agreement is a type of contract that defines the relationship between the shareholders of a company and how the company will operate.

Whereas a company’s constitution is a contract between the company and its shareholder and directors.

Why are Shareholder Agreements Important?

A shareholder agreement is important as it protects the interests of the shareholders and the company and reduces the risk of disputes or confusion. It allows the shareholders and directors of the company to customise the governance and operation of the company according to the needs of the shareholders.

A shareholder agreement generally covers more specific matters that would not be addressed in a company constitution, such as dispute resolution, exit strategies for shareholders or even how shares are to be valued.

A shareholder agreement can be drafted to either override or supplement a company’s constitution, so long that it does not conflict with any requirements set out in the Corporations Act 2001 (Cth). Whereas a company’s constitution is a ‘public’ document and is lodged with the Australian Securities & Investments Commission (ASIC), a shareholder’s agreement is a private document between the shareholders of the company and does not need to be lodged or registered.

A benefit of a shareholder’s agreement is that it can be easier to amend than a company’s constitution as the shareholders can agree to the process and requirements to amending the agreement. However, a company’s constitution will generally require a special resolution of at least 75% of voting shareholders.

What Should you Include in your Shareholder Agreement?

What to include in your shareholder agreement will be dependent on a host of factors and includes but is not limited to considerations about the nature of the company’s business, the sophistication of the shareholders and directors, the nature of the relationship between the shareholders and the size of the company’s business.

Some key issues that all shareholder agreements should consider are:

- Purpose and Objective. What is the purpose and objective of the company and shareholders? Have the shareholders and company prepared a business plan? Is it the objective of the shareholders to operate the company for long-term growth or operate the company with a view of selling the company once certain key performance indicators are met?

- Funding. How will the company be funded? Will the shareholders be required to inject capital into the company equally? What will be the terms (if any) of shareholder loans, how will new shares be issued and do existing shareholders have a first right to acquire any new shares? Importantly, what requirements will the company have when issuing dividends?

- Management. What rights will shareholders have in appointing and removing directors? Will each shareholder have a right to appoint their own director? What matters can directors decide vs what matters will require the consent of the shareholders?

- Exit. What will be the exit strategy for the shareholders? How and when can a shareholder transfer their shares in the company (e.g., voluntary transfer, transfer of death)? Will there be an agreed method in valuing shares in the company? What rights will an exiting shareholder have to tag along or draw along other shareholders on their exit?

- Disputes. What mechanisms will be in place to deal with disputes between shareholders? How will deadlocks between shareholders, breaches of the shareholders agreement or termination of the shareholders agreement be dealt with?

- Restrictions. Will the shareholders require any restrictions on shareholders in carrying on a business similar to the company? Will the remaining shareholders require exiting shareholders to agree to a non-compete upon their exit? How will confidential information and intellectual property be dealt with on the exit of a shareholder?

What to do next?

A well drafted shareholders agreement will help outline shareholder interests and rights in relation to the running of the company and will in many instances help prevent or resolve conflicts, while facilitating the growth of the business.

For more information and guidance on drafting a shareholder agreement, please do not hesitate to reach out to one of our commercial lawyers.

Written by Ariana Wu

In project finance, full recourse financing provides the Lender an “all monies” claim on the Project Sponsor’s assets, extending to all obligation owed by each borrower and each other guarantor. In some large projects, the Project Sponsor will tend to limit their responsibility and exposure in the event of default under the loan. Thus, they will tend to a different financing structure, which is known as limited recourse financing.

What is Limited Recourse Financing?

Limited recourse financing, as its name suggests, is where a Lender has a limited claim on the assets of the project if the Borrower fails to generate sufficient cash flow to repay the debt. It is often used in Project Finance or Property Finance when a Lender relies upon the cash flow and assets of the project for repayment and security, as the loan’s security is limited to certain assets and entities.

What is the Impact of Limited Recourse and Potential Risk to the Lender?

The impact of limited recourse finance is significant for both the Lender and the Project Sponsors. On the positive side, limited recourse provides protection for a Project Sponsor by shielding the Sponsor’s other assets from potential seizure and enforcement. It is preferred for those Project Sponsors who have multiple projects, because it allows each project to be completely segregated. For the Lender, the impact is twofold. Limited recourse finance can be tailored to attract more Lenders, including banks, institutional lenders, and alternative capital providers to participate in financing because their downside risk is confined to the project itself. However, it may also result in higher interest rates or stricter terms as Lenders are taking on greater risk compared to full resource financing.

In the current market, there are two approaches in limited recourse financing. One approach is the Lender lends directly to the Project Sponsor; contractually limiting the Lender’s rights of financial recourse to the rights in relation to the assets that are wholly or predominately financed or secured by the loan. The other approach is the Lender lends to a special purpose entity established by the Project Sponsor. In the second approach, the benefit is to separate the special purpose entity’s assets and liability from that of the Project Sponsor. In the event of a default, the Lender can only seek recourse on assets that are wholly or predominantly financed or secured by the loan while the Project Sponsor could possibly walk away without any further liability as the Lender takes over the asset.

In considering this type of security, the lender ought to also consider the potential risk of administration of its borrower. During the administration of a company, a financier or other third party is restricted from enforcing its security in certain circumstances by operation of Section 440B Corporations Act 2001 (Cth)[1] (Corporations Act). The restriction applies to most security interests, including mortgage and security agreements and acts as a “Arresto Momentum” charm on the enforcement of security interests during the course of the administration. The operation of the section 440B does not give the administrator a right to deal with assets contrary to a secured party’s assets, however; it is to ensure the administrator has enough time to consider the following arrangement of the administration carefully and fully.

Practically, the delay of enforcement may largely devalue the security. Section 441A of the Corporations Act also provides an exception to the statutory moratorium on the enforcement of certain rights of secured creditors holding a security interest which is perfected under the Personal Property Security Act 2009 (Cth) (PPSA), stating that a secured creditor may enforce its security interest if: 1) the creditor has a perfected security interest over the whole, or substantially the whole, of the property; and 2) the enforcement occurs within the decision period, being 13 days after the appointment of the administrator.

What is a Featherweight Security Deed

In light of the enforcement risk under potential administration, a featherweight security deed may be an option to protect the Lender’s interest in the delay of enforcing the security. A featherweight security is a “feather-like light touch” security interest which is over all assets and undertaking of a company but does not prevent dealings with the featherweight collateral unless or until an administrator is appointed. It usually operates as a floating charge and enforceable only where an administrator is appointed to the company.

The benefits to the Lender include not only minimising the moratorium risk but also helping to reduce collateral pressure and provide more flexibility in structuring. Featherweight security allows Lenders to require minimal collateral, reducing the financial burden on the Project Sponsor. Especially when the Lender is providing limited recourse financing to the Project Sponsor, the Lender’s security can still have a broader coverage with featherweight security. A Lender can benefit from the flexibility of tailoring the security arrangement to the specific needs of the project. This adaptability fosters a collateralised approach, aligning the security structure with the dynamics of the project.

The advantages to the Project Sponsors are noteworthy. the featherweight security will allow the Project Sponsor to continue its normal course of business, giving more room to retain control over its own assets. This can be vital for maintaining liquidity and supporting business activities. The flexibility may also be of importance for businesses that require utilisation of the assets efficiently to support ongoing operations. Finally, featherweight security also promotes a more balanced risk allocation between the Lender and the Project Sponsor by bearing the risk and sharing the success of the project.

It may be preferrable to the Lender to take featherweight security when providing limited recourse financing considering the benefits and advantages in its practice. Under Section 441A Corporation Act, the Lender with security over the whole or substantially the whole of the assets of the company has 13 business days following the appointment of the administrator to exercise its right under the security granted in its favour. If the Lender has featherweight security interest over all of the Project Sponsor’s assets, there is an open window of 13 business days to enforce that interest. The Lender needs to bear in mind that the featherweight security interest must then be registered on the Personal Properties Security Register (PPSR) in time. When the security is registered, it must be described the interest in a way that is clear to all parties that this security is intended to be “featherweight”.

If you require any assistance with advice regarding limited recourse financing or adopting a featherweight security mechanism into your next finance deal, JHK Legal will be happy to assist.

[1] CORPORATIONS ACT 2001 – SECT 440B

Written By Dakota Raeburn

Key Takeaways

The Property Law Act 2023 (Qld) (‘the Act’) was passed on 25 October 2023 and will commence on a date set by proclamation (to be announced in the near future). The Act is designed to replace the outdated Property Law Act 1974 (Qld), aligning the State with contemporary standards.

With the imminent commencement of the Act, Queensland property laws are set for a comprehensive makeover; the primary focus being to place paramount emphasis on optimising transparency and enhancing buyer protection within property transactions.

Significant changes include:

- Enactment of a seller pre-contractual disclosure scheme coined to ensure transparency;

- Updates to leasing regulations providing extra safeguards for existing and past lessees;

- Changes to the enforceability of covenants;

- Abandonment of the rule against perpetuities of trusts; and

- Deed-based actions subject to changed time limitations.

Mandatory seller disclosure regime

One of the most notable transformations ushered in by the Act is the requirement of a seller disclosure statement, encompassing the sale of all freehold land, inclusive of sales by auction, however exceptions do apply.

Previously, Queensland has been characterized as a ‘buyer beware’ jurisdiction, placing the onus on buyers to undertake their own due diligence. Sellers, by contrast, bore minimal responsibility for disclosing any potential issues associated with the property.

The Act marks a departure from this concept, instigating a shift toward enhanced transparency and allowing buyers to make informed decisions prior to entering into a contract. The changes will also align Queensland with other Australian jurisdictions which already require that form of disclosure.

What does a seller have to disclose?

The requisite disclosure is required to be in the approved form of a statement as well as any prescribed certificates relating to the lot. The information inputted in the statement must be true at the time it is given to the buyer and must include the seller’s signature. See the link below to view the approved form.

Examples of certificates that could accompany the statement include, but are not limited to:

- Title searches;

- Registered survey plans;

- Body corporate information;

- Community management statements (‘CMS’);

- By-laws that are not contained in CMS;

- Adjudicators orders;

- Pool compliance certificates;

- Notices from the Environmental Protection Agency; or

- Notices from the Queensland Building and Construction Commission.

When and how do disclosure documents have to be provided?

All documents are required to be provided to the buyer of a property prior to the buyer signing the contract, which may be done either physically or electronically. In relation to properties acquired through auctions, special regulations apply to ensure the disclosure is provided in a timely manner for buyers to make informed decisions.

What are the consequences of non-compliance?

In the event there is a failure on the seller’s part to provide an accurate seller disclosure, buyers may be entitled to exercise their right to termination of the contract at any time before settlement. This will arise if a disclosure statement is either not provided to the buyer or the buyer goes on to uncover ‘material inaccuracies’ concerning the property that were not initially disclosed, provided that the buyer was not aware of the correct state of affairs at the time of signing and if the buyer had the requisite awareness, the contract would not have been executed. Furthermore, that termination and a right to a refund of the deposit and any interest paid are a buyer’s only remedies. That is, there is to be no right to compensation.

What are the exclusions to the disclosure?

The framework defines several categories that are to be excluded from disclosure, including:

- Sales mandated by a court order;

- Sales between co-owners or adjacent landholders for the purpose of boundary realignment;

- Sales between related parties where the buyer willingly forgoes the requirement;

- Transfers to personal representatives or beneficiaries pursuant to a will or resulting from the death of a property owner;

- Contracts originating from an option, provided that the seller gave disclosure to the buyer upon entering the option. This is applicable solely when the buyer in both the option for the sale of the property and the contract for the sale of the property remains unchanged. If a nominee is designated under an option, distinct disclosure is obligatory before the option is exercised.

- Sales with a contract price exceeding $10 million (including GST) where the buyer willingly forgoes the requirement;

- Sales by entities like the Sunshine Coast/Brisbane City Council or another local government, aiming to recoup overdue rates or charges. In these instances, the buyer will receive a notification that the seller is not obligated to furnish the disclosure statement and necessary certificates;

- Sales by the state where the buyer has been the property’s tenant for a minimum of three years; and

- Sales involving buyers who are publicly listed corporations (or subsidiaries of publicly listed corporations), the state, statutory bodies, or constructing authorities under the Acquisitions of Land Act 1967 (Qld).

Leases

The Act also heralds a wave of leasing reforms set to elevate the legal landscape for tenants and landlords promising a more dynamic and streamlined leasing experience.

Assignment liability

A pivotal change, restricted to leases initiated after the commencement of the Act, revolves around the liability of an initial lease assignor and their guarantor when the lease undergoes subsequent assignments to new parties. The common law has previously ruled that if Lessee 1 transferred their lease to Lessee 2, who subsequently conveyed it to Lessee 3, Lessee 1 could potentially remain accountable for any default of Lessee 3. However, the Act, will ensure that at the time of the assignment from Lessee 2 to Lessee 3, there will be a release of liability of Lessee 1 and their guarantors, solely in relation to breaches of the lease by Lessee 3. In the event that there are accrued breaches by Lessee 2, Lessee 1 will remain liable, unless this obligation is expressly waived. Landlords may choose to address this modification by integrating clauses into the lease that specify that, for consent to an assignment to be granted, the assignee must furnish new guarantors or security.

Landlord consent

Another noteworthy amendment is to the obligations for acquiring consent for lease assignments or other transactions involving the lease or premises. The amendments are an extension of the prevailing principle present in the Property Law Act 1974 (Qld), ultimately reinforcing that lessors are prohibited from unreasonably withholding consent. Specifically, lessors will now have to abide by a statutory timeframe (typically one month after receiving the details of the request) to provide their decision on whether they choose to consent or not to the lessee’s request. If a situation arises in which a lessor fails to provide consent decisions, unreasonably withholds consent, or imposes unreasonable, unnecessary, or onerous conditions, a lessee will possess the right to seek damages. These provisions will apply from the date of commencement regardless of the date of entry into the lease.

Covenants in leases

The Act aims to clarify the enforceability of covenants within a lease, after a tenant’s assignment or a landlord’s reversion sale. The concepts of covenants that ‘touch and concern the land’ will no longer be relevant, instead the benefit and burden of all covenants will be held to run with the land unless:

- The lease term is explicitly stated to be personal to the parties; or

- The lease term excludes the operation of the Act; or

- The lessor and transferer or the lessee and assignee agree in writing that either the benefit of a term remains with the lessor or that the benefit of the term remains with the lessee.

Easements: Enforceability of covenants

Under the Property Law Act 1974 (Qld), positive covenants in easements generally lack enforceability against successors in title. To establish the obligatory nature of covenants within registered easements, the Act will ensure both positive and negative covenants concerning the ‘use, ownership or maintenance’ of the encumbered land are enforceable against future landowners. Provided the covenant is not expressed to be personal, the new section will apply to all easements irrespective of their creation or registration date.

Trusts: The abandonment of the rule against perpetuities

The existing common law principle against perpetuities stipulates that an interest in property must vest within 21 years following the death of a person alive at the time the interest was established. The Act substitutes this with a predetermined duration of 125 years, commencing from when the property is placed into the trust, facilitating increased adaptability in trust structuring and planning.

For existing trusts, the adoption of the new rule can be achieved either by the adjustment of the vesting date, enabled by the trustee’s authority or by formulating a new legal document with unanimous agreement from all beneficiaries. However, it must be acknowledged that potential duty and taxation implications will need to be considered when amending existing trust arrangements in response to these revisions.

Deed-based actions: Time limitations

Within the sphere of deed-based actions, the Act synchronises the limitation period with that of contract-based actions. The timeframe is set to decrease from twelve years to six years, establishing consistency across both types of commercial agreements.

How we can assist

In anticipation of the forthcoming commencement date of the Property Law Act 2023 (Qld), it is imperative for property owners and all stakeholders involved in property transactions to have a comprehensive understanding of their responsibilities. Our team at JHK Legal are well-versed in the intricacies of the Act and look forward to providing expert guidance on interpreting, applying and complying with the new regulations.

(more…)Written by Hanaa Merhi

What is a statutory demand?

In Australia, a statutory demand is a formal request for payment of a debt that is owed by a company. Statutory demands are issued under section 459E of the Corporations Act 2001 (Cth) (Act).

If you’ve been served with a statutory demand, you should seek legal advice immediately as strict statutory time frames apply. If a debtor company fails to comply with a statutory demand within 21 days of service, a presumption of insolvency may exist, and the Company may face the possibility of being wound up by order of the court. So, it is important to know your rights if you are served with one.

When a company is insolvent, it means the company cannot pay its debts as and when they fall due. In these instances, creditors of the debtor company can take various steps to enforce their rights. That includes serving statutory demands.

If you are served with a statutory demand, you can choose to either:

- Pay the requested figure within the 21 days after being served;

- Negotiate a settlement for the debt with your creditor; or

- Set aside a statutory demand via a court application. For example, in the event of a genuine dispute about the debt claimed or where a defect may exist in the demand that would cause substantial injustice to the debtor.

If a debtor company fails to undertake any of the three actions within the statutory period, it will be presumed insolvent. The creditors can appeal to the court for the debtor company to be wound up. A liquidator will be assigned to the debtor company to begin liquidation proceedings.

When can a statutory demand be made?

A creditor can issue a statutory demand if:

- The debtor in question is a company;

- If the creditor is owed at least $4,000;

- If the debt is due and payable; and

- There is no genuine dispute about the debt.

A valid statutory demand must meet the following requirements:

- It is in writing and uses the prescribed form, which is Form 509(H);

- It accurately specifies the debtor company and the creditor(s);

- It is signed by the creditor making the statutory demands or their agent;

- The statutory demand states the name of the debtor company to which the statutory demands are made. This includes the company’s registered office address;

- The statutory demand specifies the amount of debt owed; and

- It must detail a location in Australia where the debt may be paid. This usually takes place at the debtor company or their legal practitioner’s office.

How is a statutory demand served?

A statutory demand may be served either personally or by post. If you are registered as a company in Australia, the statutory demand must be served to your company’s registered office address.

What happens if I don’t respond to a statutory demand?

Ignoring a statutory demand is not a recommended course of action. It is essential to address the situation promptly to minimise the potential legal and financial consequences.

If the Company fails to comply with a statutory demand within 21 days, then the Company will be presumed to be insolvent. The company or person who served the statutory demand can begin a winding up application against your company on the basis that your business is insolvent.

If you’re served with a statutory demand, it’s important to act quickly while you still have options available to you. If the 21 day time limitation for compliance with a statutory demand lapses without any of the abovementioned options being exercised, then the creditor may rely on the presumption of insolvency to commence a winding up application, to wind up the Company in insolvency.

If you are served with a statutory demand, you should seek out legal advice as soon as possible. You may be able to challenge creditors’ statutory demands if you have grounds to do so.

On what grounds can I set aside a statutory demand?

If you have been served with a statutory demand, and you believe that the debt is in genuine dispute, or that you have an offsetting claim, then you can apply to the court to set aside the statutory demand. To successfully set aside a statutory demand, you must demonstrate to the court there is a valid reason for the statutory demand to be set aside.

The most common grounds to set aside a statutory demand are:

- The debt claimed in the creditor’s statutory demand is in genuine dispute.

- You have an offsetting claim, and this claim reduces the amount of the debt claimed in the statutory demand to less than the statutory minimum.

- The statutory demand is defective.

The Company must file an application within the 21 days of being served with the statutory demand. It’s important to act quickly, as this is a serious matter that could lead to the winding up of the Company. If you’re not sure what to do, seek legal advice as soon as possible.

Can a statutory demand be withdrawn?

Yes, if there are grounds for the debtor company to set the statutory demands aside. The creditor may be informed of reasons for withdrawing the statutory demands (for example, if there is a genuine dispute), and be asked to withdraw it.

The withdrawal of statutory demands can be done either in oral or written form. However, a debtor company should always have a written copy of the withdrawal, in case they need to refer to it in the future.

Creditors may still opt to dismiss the debtor company’s request to withdraw a statutory demand. However, if the company succeeds in petitioning the court to set its statutory demand aside, the creditor may be ordered to cover the costs of setting it aside.

If your company has been served with a statutory demand, time is of the essence, and it is crucial that you obtain legal advice as soon as possible.

Please contact JHK Legal if your company has been served with a statutory demand or if your company wishes to issue a statutory demand against a debtor company. If you have any questions, please contact our office.